Foreign Direct Investment in 2026: Challenges, Opportunities and the Road Ahead

20/01/26

Foreign Direct Investment (FDI) has long been a cornerstone of global economic integration, driving growth, innovation and job creation. As we enter 2026, however, the FDI landscape is undergoing profound change. Shaped by geopolitical realignment, rapid technological transformation, climate priorities and evolving regulatory frameworks, global investment flows are increasingly guided by factors beyond cost efficiency and market access.

Crucially, it is not just what is changing but the speed, scale and scope of change, reshaping FDI risk and opportunity. Investors face faster-moving policy shifts and system-wide transitions affecting entire sectors, alongside a broader set of political, security and sustainability considerations. For governments, investors and multinational companies, this represents both heightened uncertainty and opportunity and navigating this environment will be critical to sustaining long-term investment and development.

Key Challenges for FDI in 2026

Weak Global FDI Flows

Despite recovery in some regions, global FDI remains below its pre-pandemic trajectory. Investors are more cautious, prioritising balance-sheet resilience and shorter payback periods. Long-term, capital-intensive projects, particularly in infrastructure and traditional manufacturing have been slower to recover.

Rapid economic and policy shocks have heightened sensitivity to downside risk, making long-horizon investments harder to justify. This is especially concerning for developing economies where FDI plays a central role in infrastructure financing, industrial upgrading and employment. The result is a concerning widening investment gap between advanced and emerging markets.

Geopolitical Fragmentation

Geopolitics has become a central factor in investor decision-making. Strategic competition between major powers, regional conflicts and economic security concerns are reshaping cross-border capital flows. Investors need to assess political alignment between home and host countries, exposure to sanctions or trade restrictions and risks linked to critical technologies, data and supply chains.

The scale of geopolitical change means that these risks are no longer isolated or country-specific, potentially affecting entire regions or sectors simultaneously. As a result, FDI is becoming increasingly regionalised, with capital flowing preferentially among politically aligned or ‘trusted’ markets. Whilst this can reduce certain risks, it also constrains capital mobility and raises costs.

Expanding FDI Screening and Regulatory Complexity

Governments worldwide, have expanded foreign investment screening mechanisms, particularly in sectors such as technology, energy, defence, telecommunications and critical infrastructure. Whilst designed to protect national security, they also add complexity and uncertainty for investors.

Approvals increasingly involve multi-agency reviews, longer timelines and conditional approvals or post-investment monitoring. For investors, the challenge is not only compliance but also unpredictability. Faster regulatory change and broader security definitions make approval risk harder to assess upfront. For small and medium sized firms, these costs and uncertainties can act as a deterrent, reducing overall investment activity.

Declining Investment in Development-Focused Sectors

Whilst high-tech and strategic industries attract significant attention, FDI into basic manufacturing, agriculture, transport, water and social infrastructure continues to lag. These sectors are vital for inclusive growth and sustainable development, particularly in low- and middle-income countries.

Large-scale transitions in technology and climate policy are concentrating capital in a narrower set of industries. Without targeted policy support and risk-sharing mechanisms, this trend risks leaving large parts of the global economy behind.

Macroeconomic and Financial Uncertainty

Although inflation has eased in many economies, financing conditions remain tight. Higher borrowing costs, volatile exchange rates and uncertain growth prospects continue to weigh on long-term investment planning.

Both the speed and scale of change has increased macroeconomic volatility, encouraging firms to balance expansion with financial discipline, and to favour incremental investments over large greenfield projects.

Opportunities for FDI in 2026

Despite these challenges, the global investment environment also presents significant opportunities for those able to adapt:

Supply Chain Diversification and new Investment Hubs

Companies are actively restructuring supply chains to reduce dependency on single markets and improve resilience. This ‘nearshoring’ trend is creating FDI opportunities in regions like Southeast Asia, South Asia, Latin America and parts of Africa. Countries that offer political stability, competitive labour markets, improving infrastructure and clear investment frameworks are well positioned to attract diversified manufacturing and logistics investment. Flexibility and speed in policy response are becoming key competitive advantages.

Growth in Digital and Technology-Driven FDI

Digital and technology-driven FDI remains a key growth area. Investment in data centres, cloud services, fintech, artificial intelligence and digital platforms continues to expand across both advanced and emerging economies, offering lower physical infrastructure requirements, faster scalability and higher value-added employment. For host countries, attracting digital investment also supports skills development and integration into global value chains.

Renewable Energy and Green Investment Momentum

Climate commitments and energy security concerns are accelerating FDI into renewable energy, clean technology and sustainable infrastructure. Solar, wind, battery storage, green hydrogen and electric mobility projects are attracting record levels of interest. Given the scale of the energy transition, countries with clear climate strategies, stable regulatory frameworks, and bankable project pipelines are emerging as preferred destinations for green FDI. Sustainability is no longer a niche consideration – it is central to investment strategy and risk management.

Emerging Markets As Sources of FDI

An important shift in recent years is the rise of emerging economies as sources, not just recipients, of FDI. Firms from Asia, the Middle East, and parts of Latin America are increasingly investing abroad to access technology, brands and new markets. This trend reflects the growth of a multipolar global investment system, creating opportunities for South-South investment flows, regional integration and new forms of partnership.

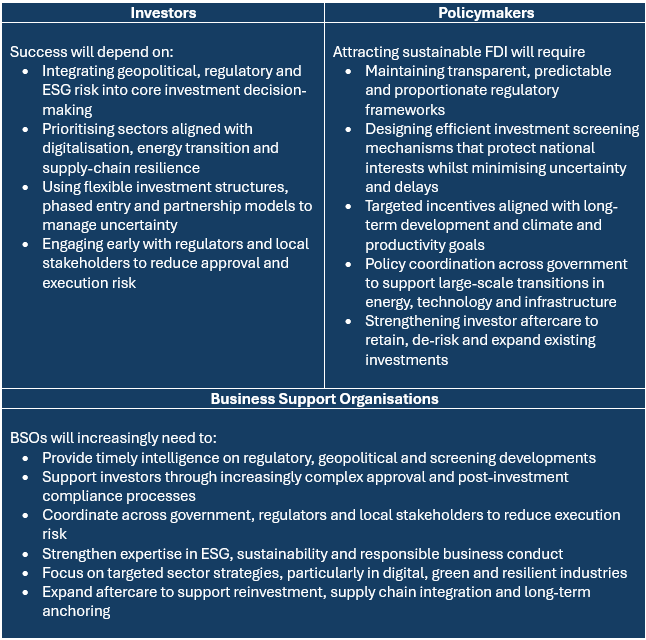

What This Means for Investors, Policymakers and Business Support Organisations

As FDI becomes more risk-sensitive and complex, effective collaboration between investors, BSOs and policy makers will be essential in sustaining investment flows and maximising development impact.

Conclusion

FDI in 2026 is not in decline, it is in transition. The speed of change, systemic shifts and a broader set of strategic, technological and sustainability priorities are rewriting the rules of global FDI.

Whilst the environment is more complex, it also offers significant opportunity. Business Support Organisations will have a critical role to play in managing the new dimensions of risk created by the speed, scale and scope of change.

Investment ecosystems that are able to adapt, embrace flexibility and cooperation, whilst aligning policy, promotion and investor support around long term resilience and sustainable growth will be best placed to thrive in the next phase of global Foreign Direct Investment.

If you would like to discuss how MSI can support you in navigating these changes, please do not hesitate to contact us.